In *most* markets nationwide, we have seen a continued freeze on transactions. Many potential buyers are waiting to see what the Fed will do, whether there will be civil unrest surrounding the election, and if new home builders have potentially overshot development needs in some geographies. There is a general sense of discomfort and unease that we hope will dissipate by November.

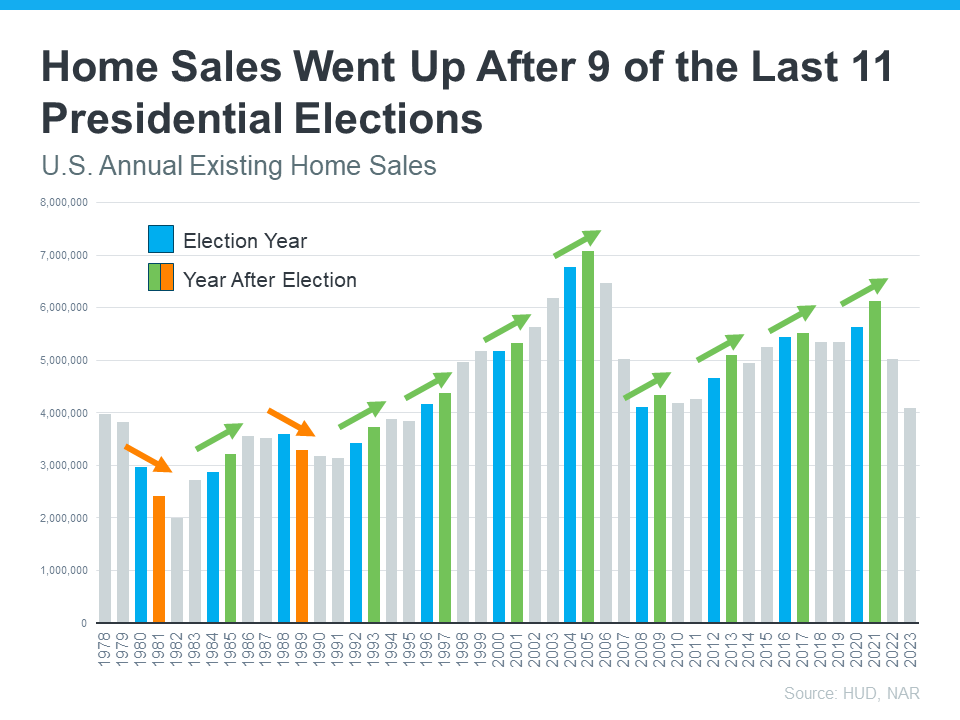

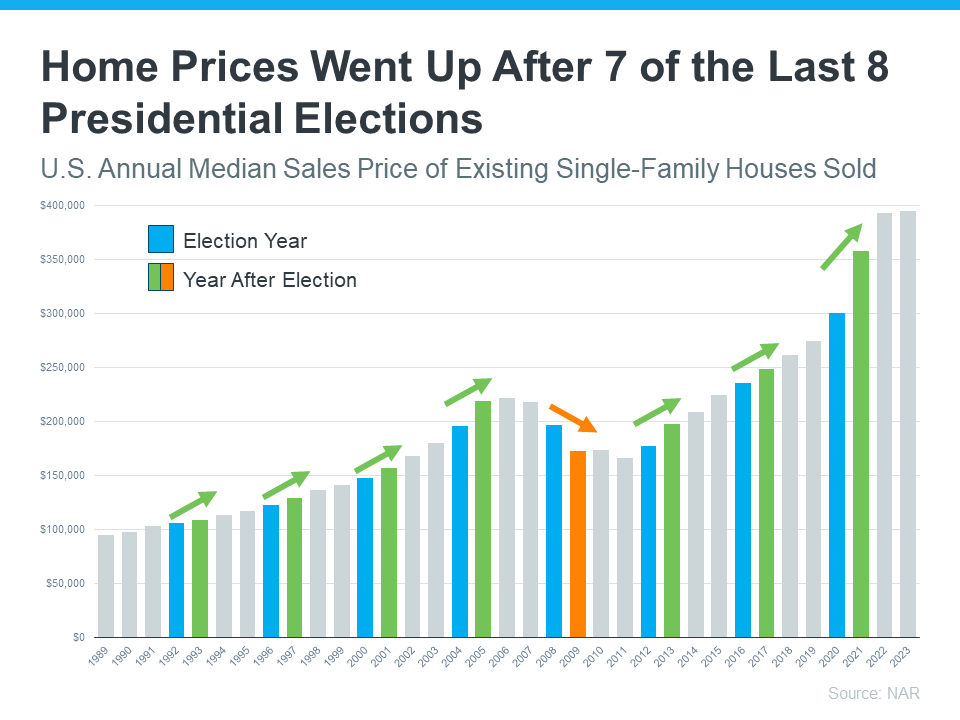

Historically, there are further slowdowns in home sales during the month of November in Presidential election years. That said, things are likely to shift as we move into 2025, as existing home sales have increased in the year following 9 of the last 11 Presidential elections AND home prices went up in the year after 7 of the last 8 Presidential elections.

In the Palm Beach market (which I note often is moving ahead of the national curve), Mar-a-Lago is oceanfront and center, and a Trump re-election would likely reignite local real estate activity. At present, single family home prices on the island are down 31.8% y/y, thus, this summer may be the last opportunity to take advantage of discounts and extended days-on-market. While there have been some notable mega sales on Palm Beach recently, transaction volume has been inconsistent across all price points.

Historically, the Fed has tried to avoid making major monetary policy decisions too close to an election. However, it seems that the invisible hand may be politicized, with the first rate cut coincidentally expected in September. Though this cut is not guaranteed, it has already been priced in to home builder stock prices and even current mortgage rates, which are currently hovering around 6.8%, a full point lower than last year’s peak.